.png)

Dear Patron,

Contrary to general notion, negativity bias is in fact a good thing. It is an important factor that has ensured survival of the fittest. Our hunter-gatherer ancestors survived by being extra conscious to any perceived threat and reacting to that instantly with agility. However, the pace of evolution over the last few centuries has been so quick that while Human Beings have evolved a lot, some of our basic instincts – from our hunter-gatherer ancestors, still drive us. (There’s a reason why that Cheececake feels irresistible) While survival may not be that big an concern now, our basic instincts of survival ensures that we do not ignore to negative in any situation and spot that first! But it has its downsides.

This brings us to the March Madness, when events during this month over the last four years have tested the grit and resilience of people at large (2020: COVID Wave 1, 2021: Wave 2, 2022: Russia-Ukraine War, 2023: a looming SU regional banking collapse). It is but normal for us to be anxious and fear the worst, especially amidst a barrage of negative events such as Mass protest in Israel, US regional bank collapse, Credit Suisse’s forced sale to UBS, Russia’s plans to station tactical nuclear weapons in Belarus, rising COVID cases in India, Mass job layoffs, etc. However, we feel that all is not that bad and there are positive news and events as well that are happening but have fallen off the front page. The moment people start paying attention to these will be the inflection point of an upwards swing.

In this newsletter we are highlighting some of the positive developments taking place that often get missed amidst the barrage of negative news. While these may be subtle as yet, but there will be an inflection point when investors will start seeing this and the mood will turn around quickly, as was seen 3 years back.

The Glass Half Full –

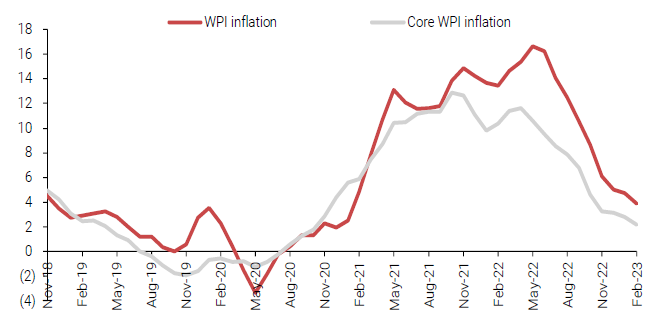

1. Interest rate cycle at an inflection point – The sporadic resumption post-COVID lockdowns resulted in supply chain bottlenecks and increased liquidity led to inflation. This saw inflation touching decadal high in US and UK. While India was much insulated, courtesy our agrarian economy, we too faced a brunt in terms of increased input costs as this is an extremely Globalized era. However, as recent trends suggest, CPI / WPI data is cooling off. Companies are confident of recovering margins. This further implies that the interest rate cycle may have peaked as no hawkish rate hikes are expected by the US fed . This should lead to yields cooling off.

Exhibit 1: India headline WPI and Core inflation is falling rapidly

Source: CEIC, Ambit Asset Management

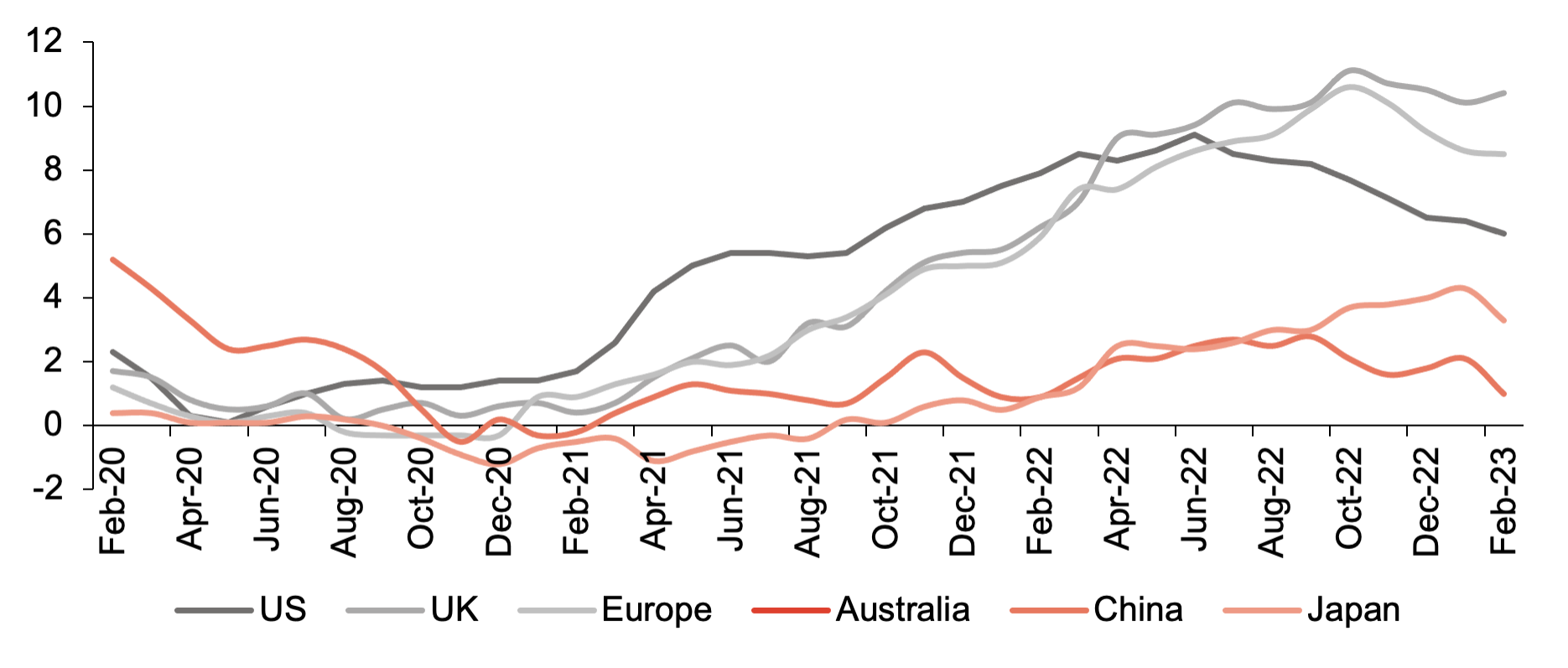

Exhibit 2: Inflation across major economies too seem to be cooling off as supply chain normalizes and base effect catches up

Source: Bloomberg, Ambit Asset Management

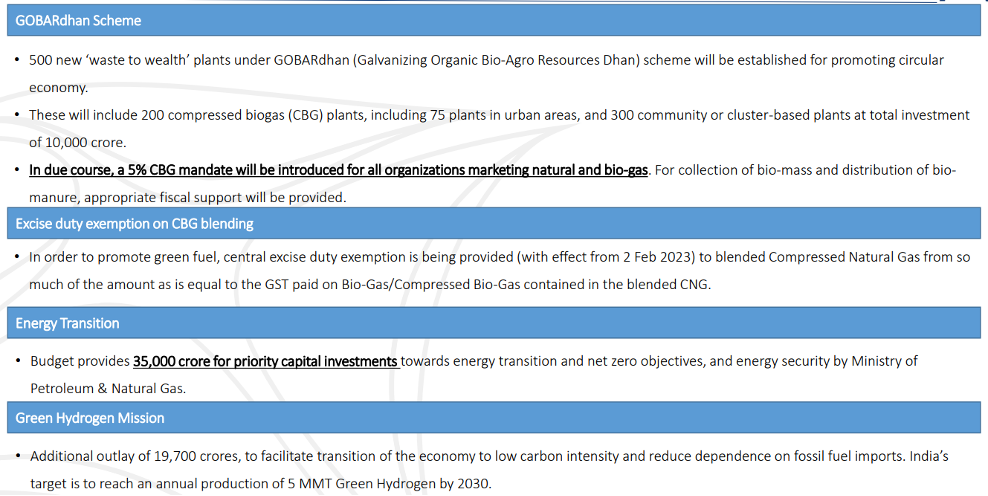

2. Focus on clean energy and healthy currency! – Brent Crude is currently trading at ~$85/bbl which is lower than RBI and Government estimates of $95-100/bbl, thus providing comfort on Current Account Deficit. While this may provide respite to our currency and economy in the near term. The bigger positive we feel – which is not much talked about – is the government initiatives to promote clean energy, especially Ethanol Blending, EV push, focus on Clean energy and Green Hydro. The recent announcements on this front in Union Budget 2023 were encouraging (Refer to Exhibit: 3) While these will help India reduce its crude import bill and dependency on the same, contain CAD and go a long way in making our country self-reliant.

Exhibit 3: Key points from Union Budget 2023 on areas of sustainability

Source: Praj Industries presentation, Ambit Asset Management

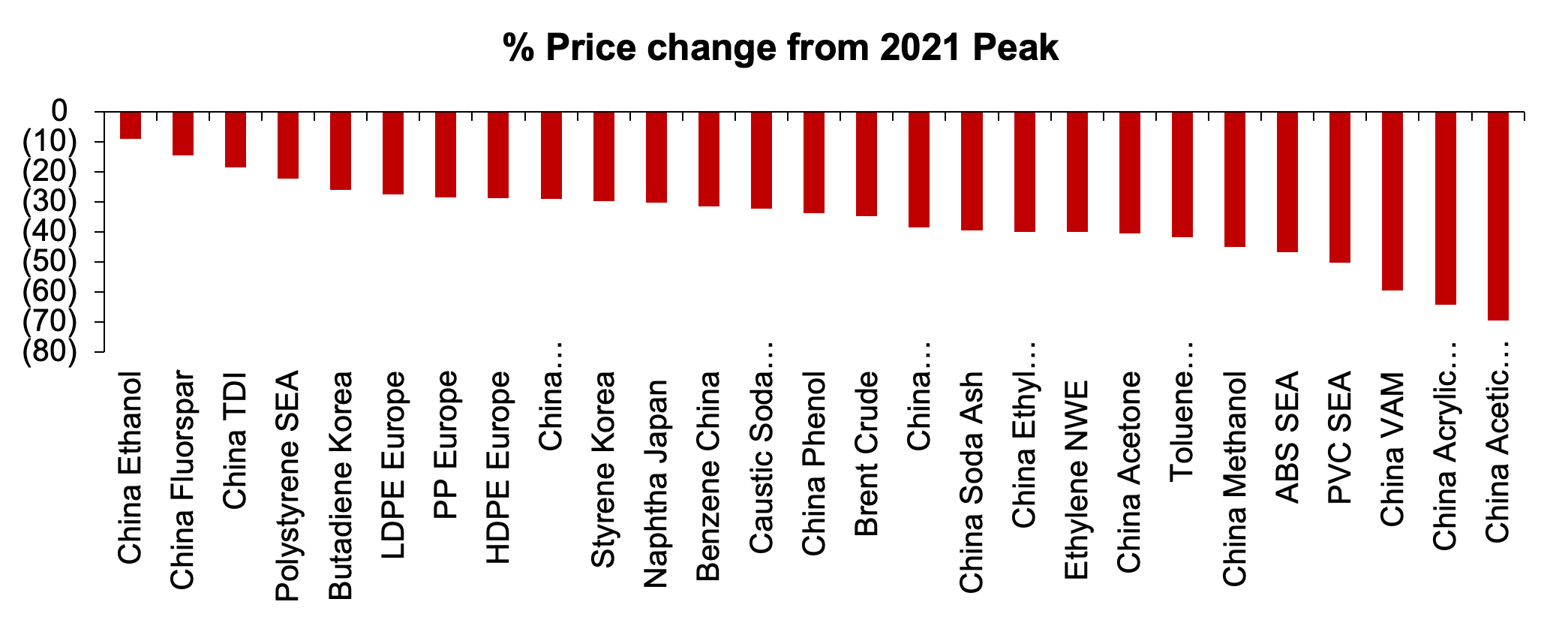

3. Easing Supply chain and input prices – Increase in key input prices, especially chemicals, as China stuck to its zero COVID policy weighed down on corporate profitability. However, prices of most of these raw materials have come off sharply since their 2021 peak (Refer to Exhibit: xx). This should help corporate profitability in a major way heading into FY24. Even freight prices, which saw a sharp increase post-COVID opening, have eased off as container availability improved and supply bottlenecks eased.

Exhibit 4: Key Raw Material price trend in Chemicals

Source: Bloomberg, Ambit Asset Management, * Cumulative outflow from Indian Equities by FII since Oct 2021

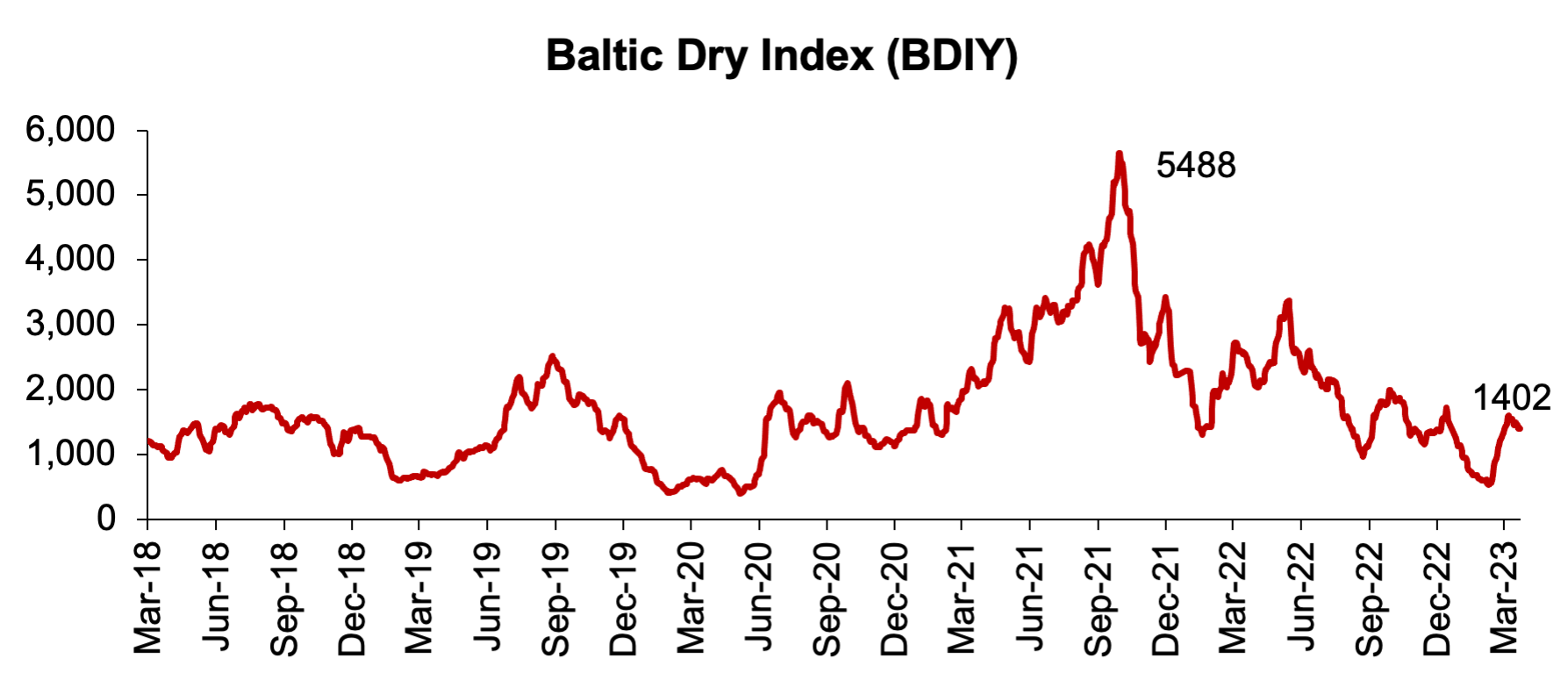

Exhibit 5: Baltic Dry Index (BDIY) which is a leading indicator of freight rates – is down ~75% from its 2021 peak

Source: Bloomberg, Ambit Asset Management, * Cumulative outflow from Indian Equities by FII since Oct 2021

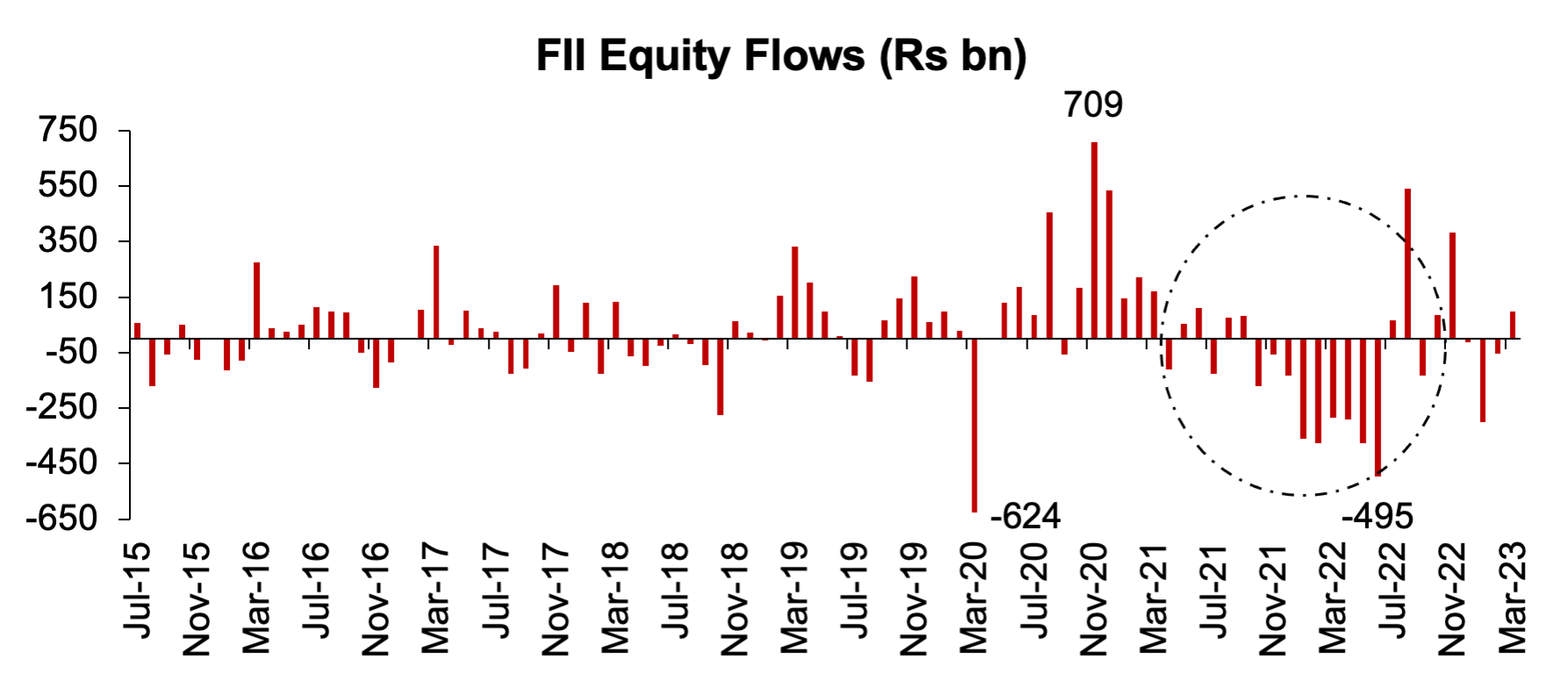

4. Indian Markets withstood one of the sharpest FII selling phase – Courtesy the Indian Domestic investors, our markets have withstood an unprecedented pressure of FII selling (Refer to Exhibit: xx).

Exhibit 6: Oct-21 to Jun-22 saw cumulative FII selling of ~Rs2.5tn – a unprecedented scale which was not witnessed in the past – despite this NIFTY50 held strong declining ~9%

Source: Bloomberg, Ambit Asset Management, * Cumulative outflow from Indian Equities by FII since Oct 2021

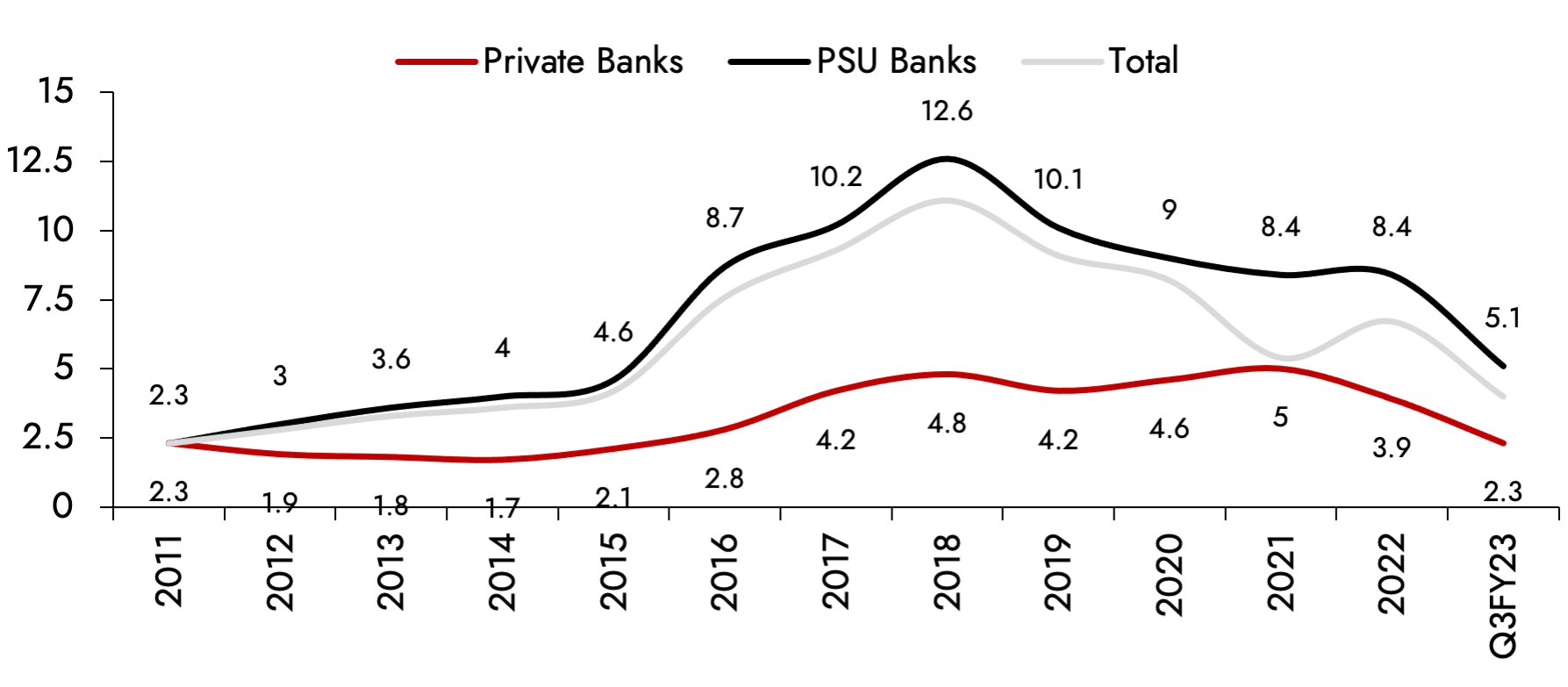

5. Resilient Indian banking system– Stability of the banking system is on everyone’s mind post the US Regional Bank challenge and Silicon Valley Bank collapse, given that banking contagion spreads much quickly, if not tackled proactively. Similar concerns arose on the Indian Banking system, which we feel is far resilient and well insulated from shocks similar to what were witnessed in the US largely owing to the proactive steps by the RBI.

Exhibit 7: Our banking system asset quality is fare resilient than it was at the peak of NPA cycle

Source: Company, Ambit Asset Management

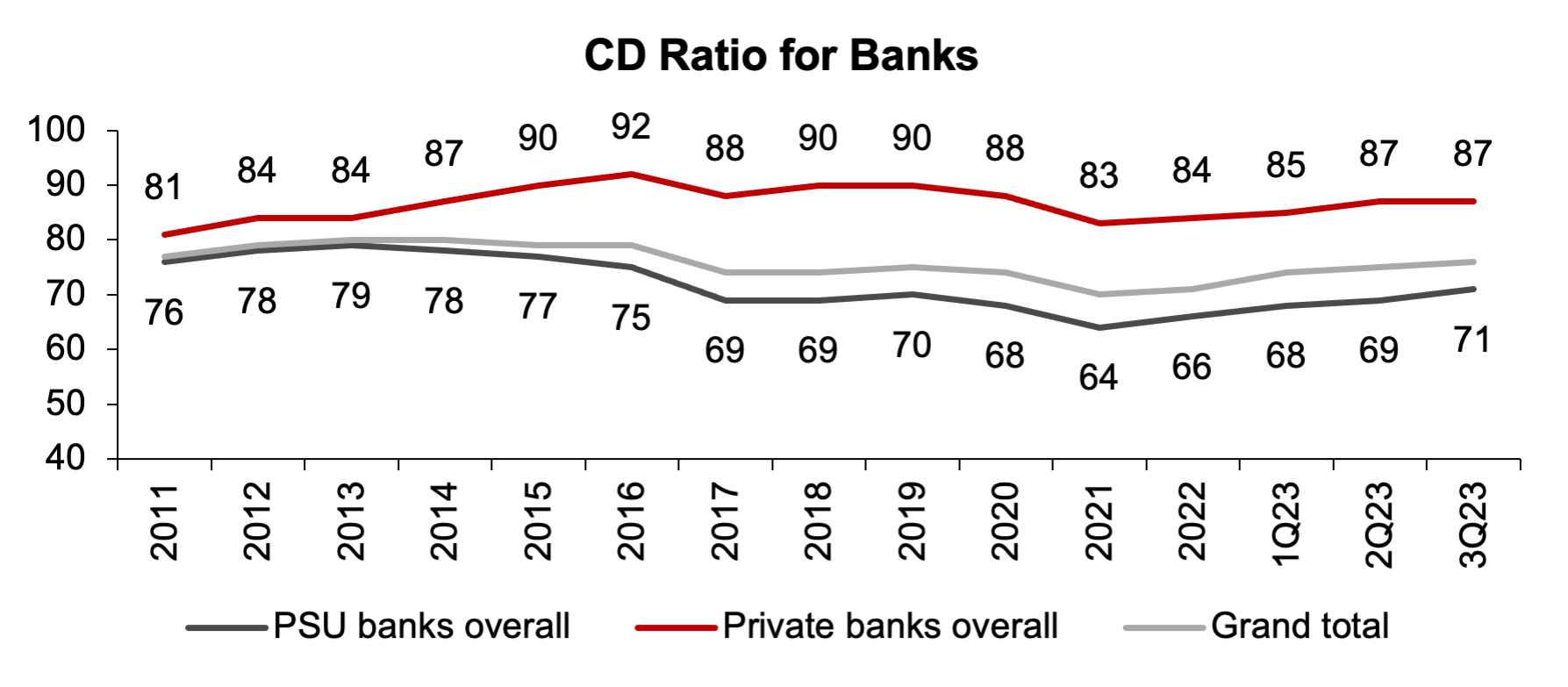

Exhibit 8: Indian banks, especially PSUs, are maintain a decent headroom on Cost Deposit Ratio

Source: Company, Ambit Asset Management

Conclusion – Tough times never last, Tough investors do!

Factors such as – Brent Crude above $100/bbl, WPI Inflation in double digit, +250bps RBI rate hikes, all in one year – would have usually had a much sharper impact on the Indian economy and the markets But thanks to the reforms and efforts taken over the last few years, the Indian Economy was far more resilient. This is something which often gets missed amidst the barrage of gloom and doom. We were in a similar situation in 2020, when the world seemed to have been ending (literally). At that time, we had highlighted some green shoots, and advised investorsto hang in there. The current situation does not seem easy, however, we believe that there are many positive indicators as well which are getting overlooked amidst the fear. Capitalizing and navigating through these is when multi-bagger returns are generated!

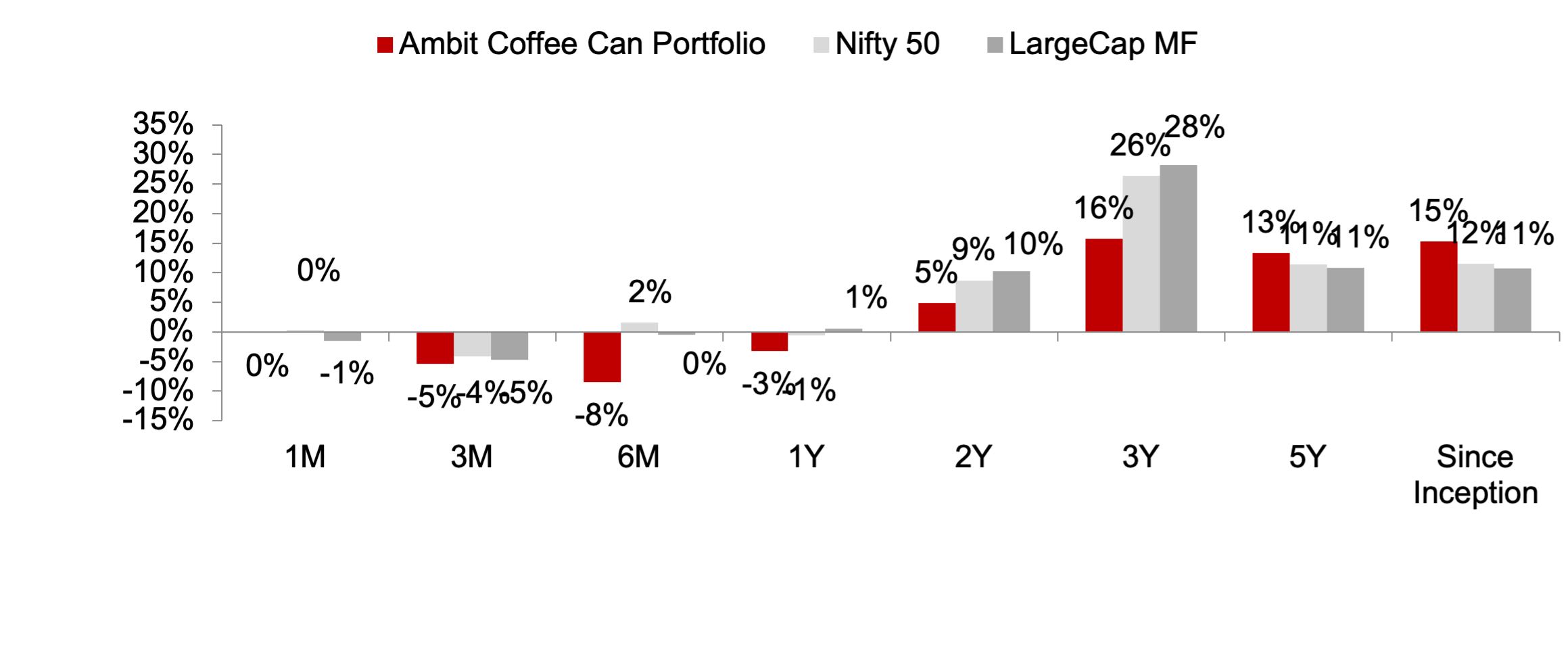

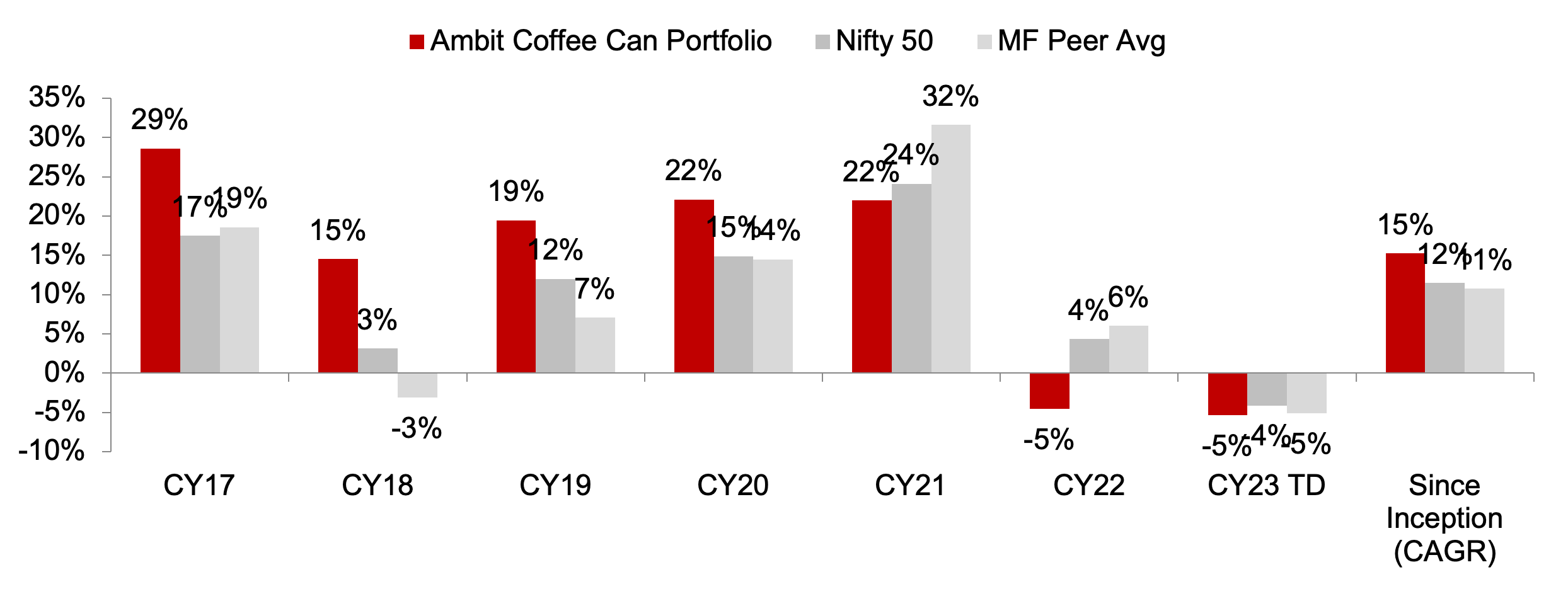

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 9: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of February 28, 2023; All returns are post fees and expenses; Returns above 1 year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

Exhibit 10: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of February 28, 2023; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

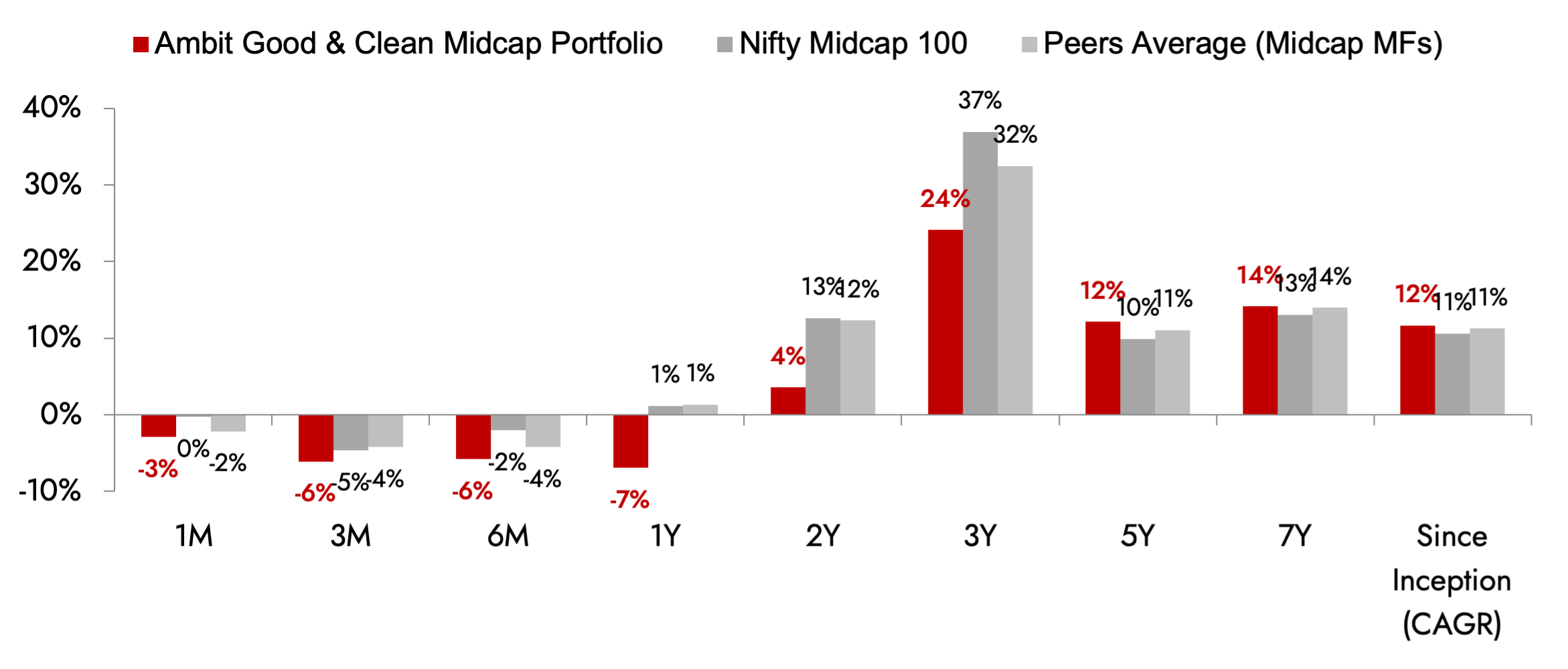

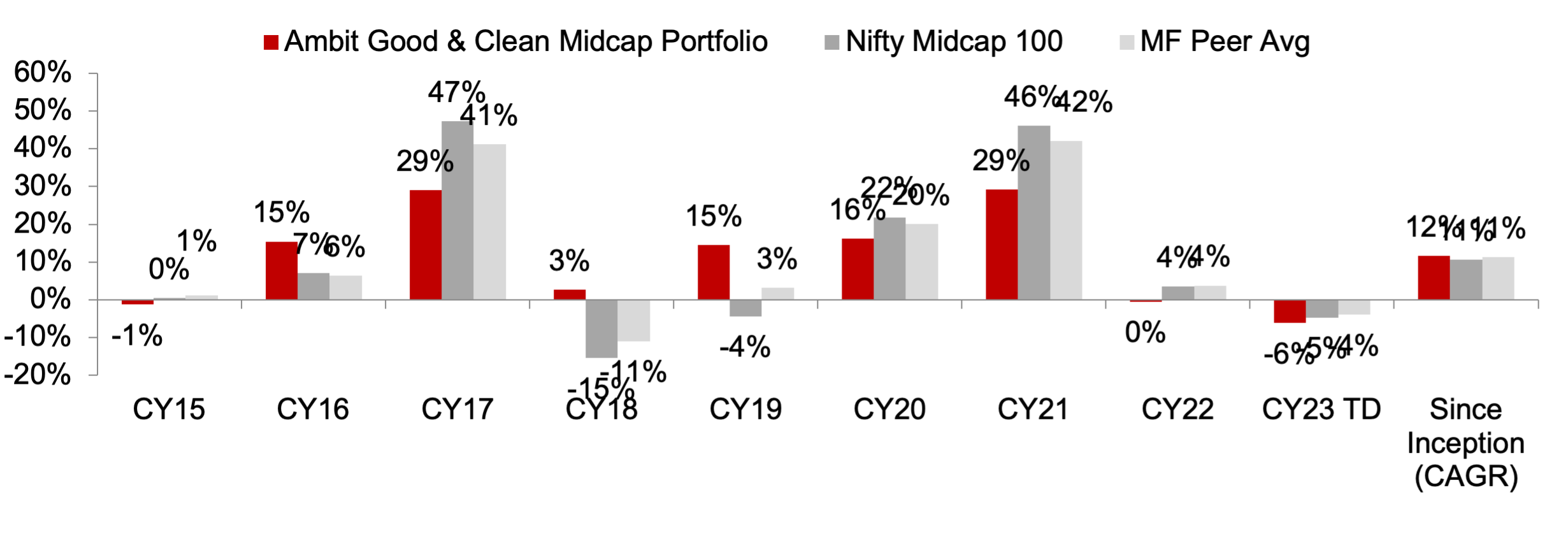

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 11: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of February 28, 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 12: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of February 28, 2023. Returns are net of all fees and expenses

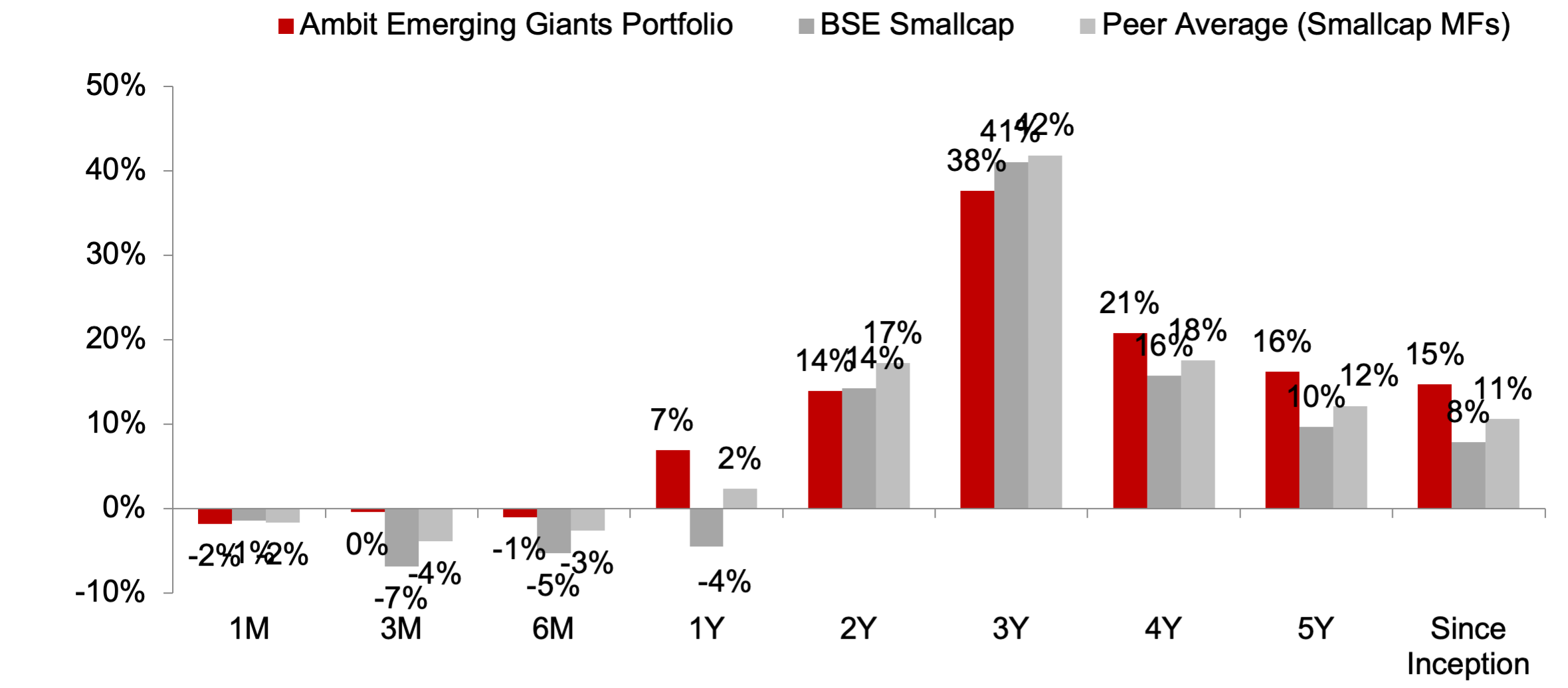

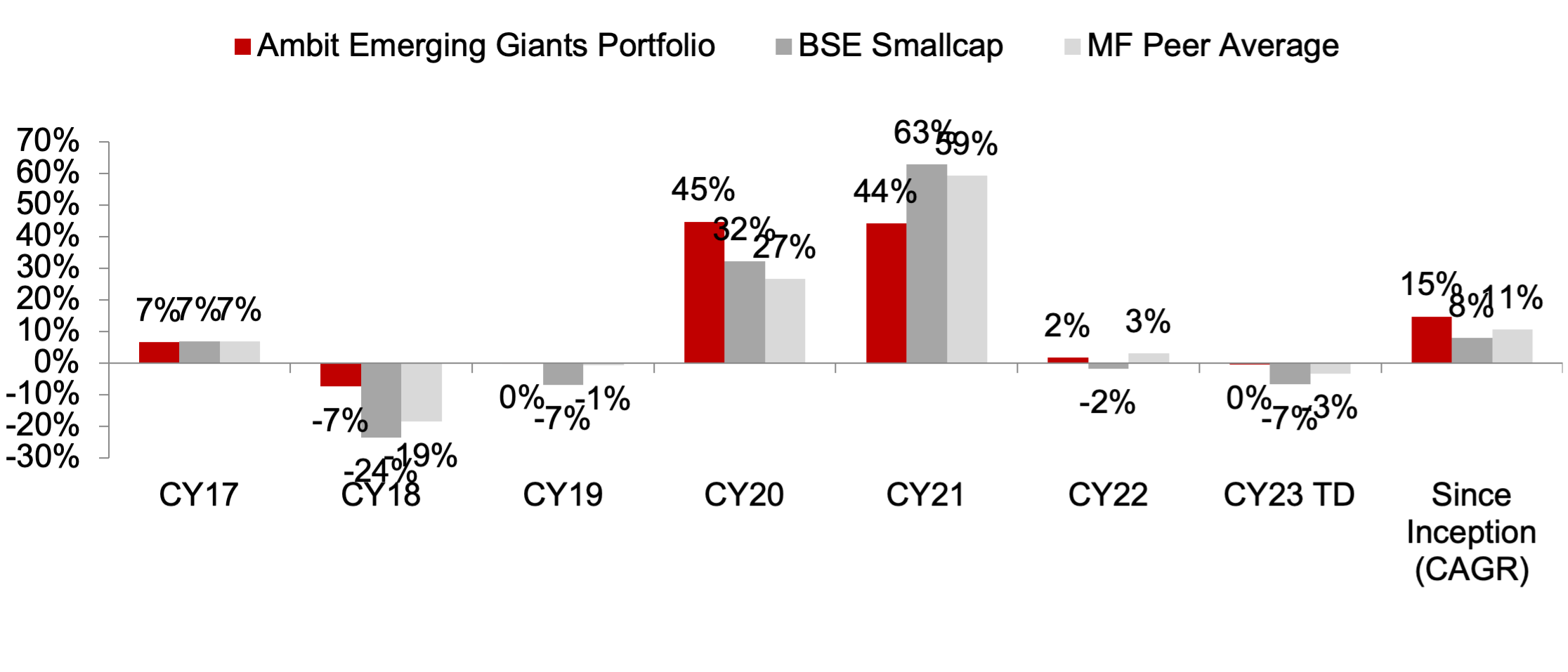

Ambit Emerging Giants Portfolio

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 13: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of February 28, 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 14: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of February 28, 2023. Returns are net of all fees and expenses

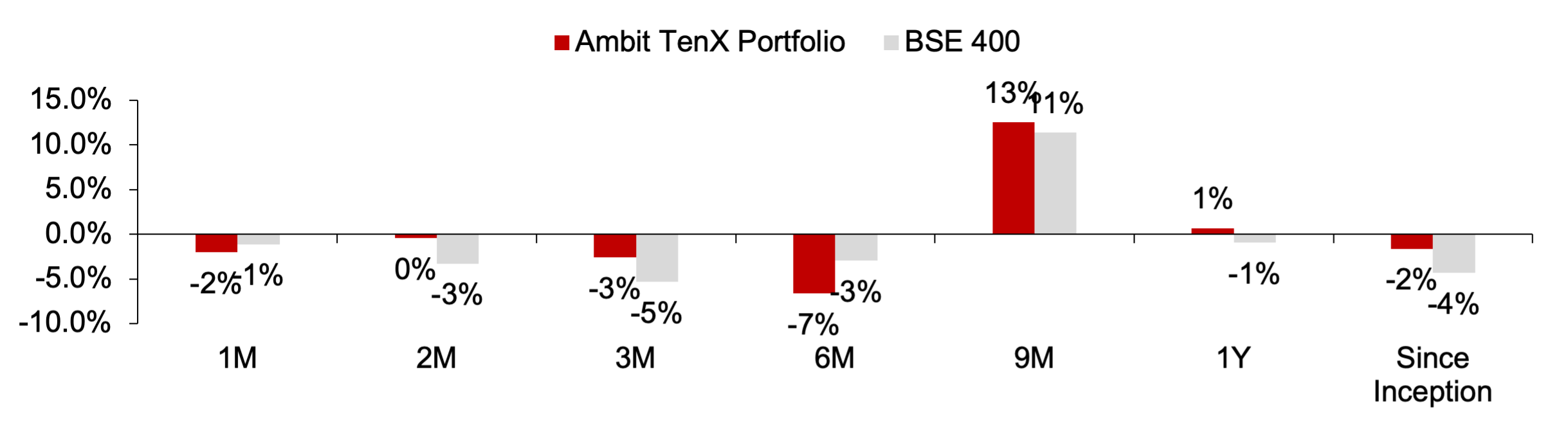

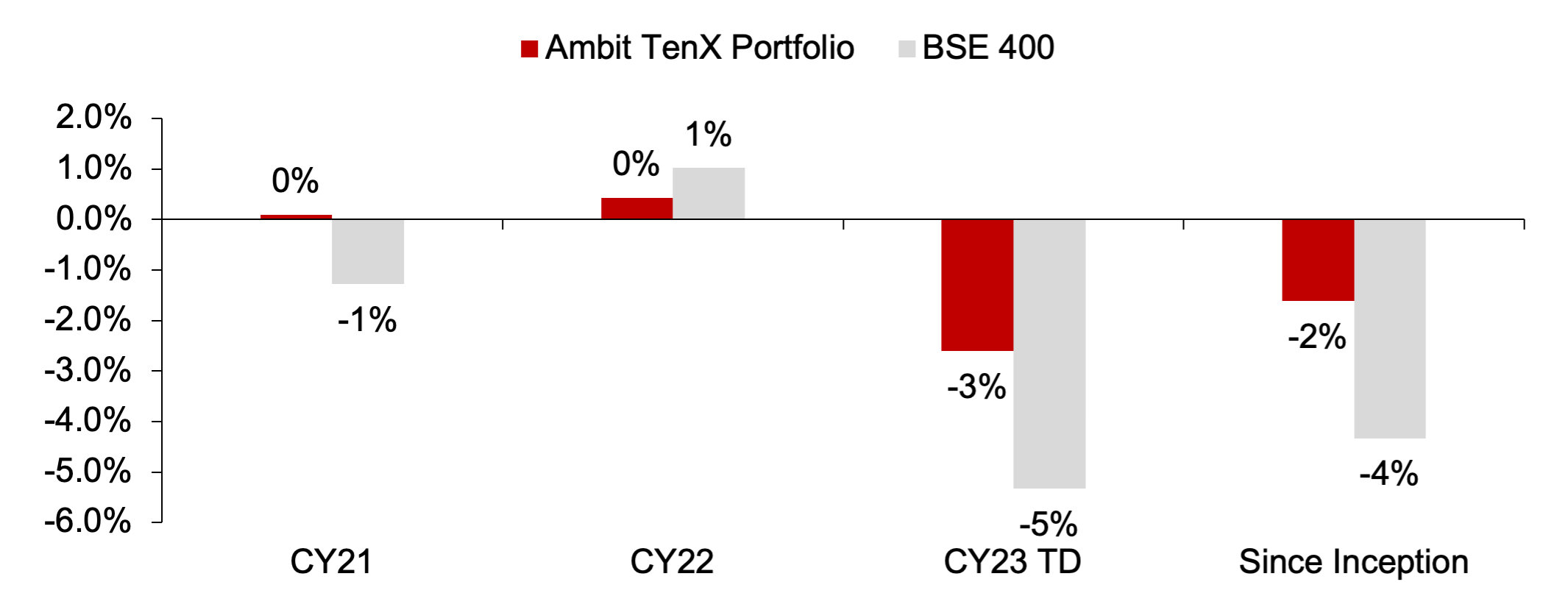

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 15: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of February 28, 2023; Returns are net of all fees and expenses

Exhibit 16: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of February 28, 2023. Returns are net of all fees and expenses

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - aiapms@ambit.co| Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020